Hi,

This is Ayaan Shah from Nextrope’s consulting department. Thank you to all of our readers for your continued support and engagement of our newsletter as we got 724 new views and 4 comments last week. We also welcomed 23 new subscribers and hope that many more people are able to gain value from our newsletter.

Our previous newsletter explored the drawbacks of the blockchain industry and identified regulation as one of the greatest challenges that individual blockchains face. This week, we will dive deeper into the topic of blockchain and cryptocurrency regulation. Where do we stand today and what progress is being made? I spoke with Professor Rasa Karpandza, who teaches fintech at NYU, on the topic as well and he had some insights to share, some of which I have mentioned in the main body of the newsletter.

Today we’ll discuss:

📈 Current regulatory ecosystem

🔺 The need for regulation

❗️ Recent regulatory actions

❓ Barriers to new regulation

If you have any questions, please don’t hesitate to ask as I am happy to answer them. Also, if you are working on any fintech or blockchain projects and would like to be featured on our newsletter, please reach out to me - a.shah@nextrope.com

Not financial advice

We have done our best to ensure that the information provided in the Newsletter and the resources available for download are accurate. However, the information contained in this Newsletter and the resources available for download are not intended as, and shall not be understood or construed as, financial advice.

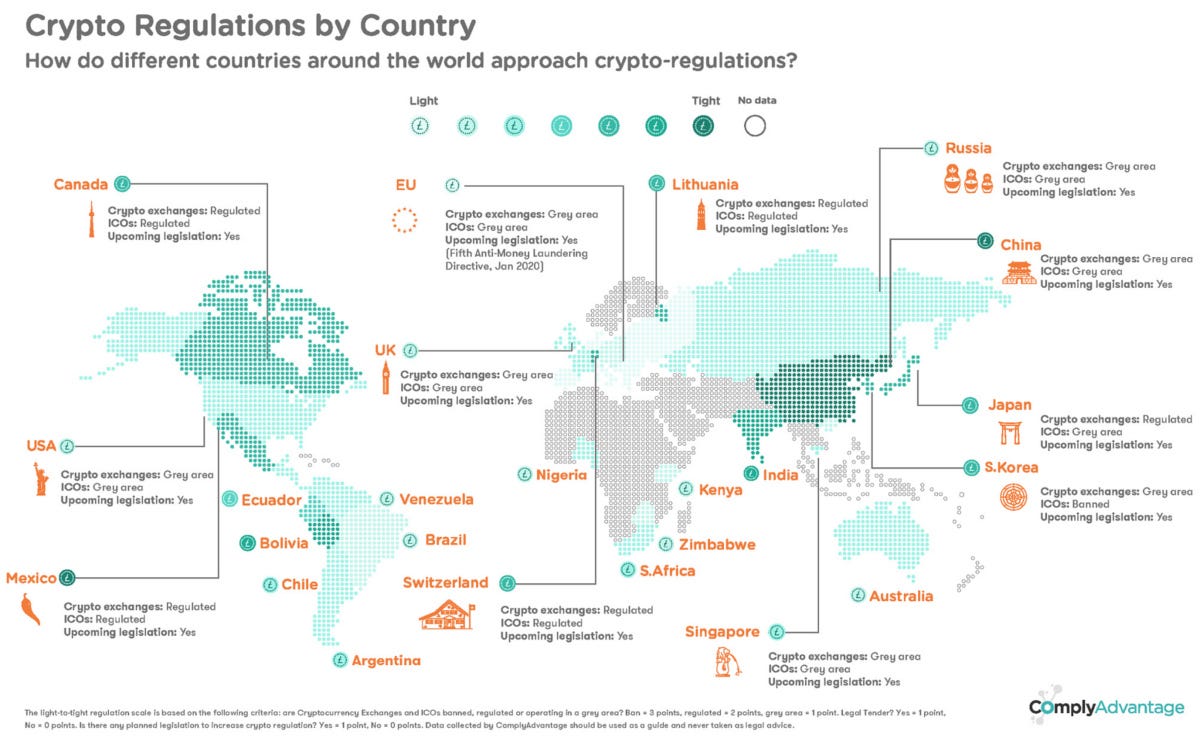

The Status-Quo of Crypto Regulation

As can be seen in the infographic below, different governments are developing varying approaches to the regulation of cryptocurrency, as its decentralized nature prevents a single, overarching method for government control.

Source: Visual Capitalist

Upon researching the regulations on blockchain in various countries, I found that countries could be split into various categories on a spectrum ranging from a complete gray area in terms of regulation to well defined rules which safe-guard investors and encourage adoption of blockchain.

On one end of the spectrum lie Algeria, Bolivia, Morocco, Nepal, Pakistan, and Vietnam. These countries have banned any and all activities involving cryptocurrencies, including trading on exchanges and issuing tokens. Qatar and Bahrain stand close by in the spectrum, though they allow their citizens to engage with cryptocurrency outside their borders.

Another group of countries such as Bangladesh, Iran, Thailand, Lithuania, Lesotho, China, and Colombia lie further away from the countries above, as they have not explicitly banned any aspect of cryptocurrency. However, these countries have barred financial institutions within their borders from facilitating transactions involving cryptocurrencies, thereby rendering them almost useless.

Standing in the middle of the spectrum are countries including Australia, Canada, and the Isle of Man. These countries have expanded their laws against money laundering, counterterrorism, and organized crimes to include cryptocurrency markets. The law also requires banks and other financial institutions that facilitate cryptocurrency markets to conduct due diligence requirements. Still, these countries have not placed any other restrictions on crypto use.

Spain, Belarus, the Cayman Islands, and Luxembourg lie further on the loose regulation side of the spectrum. They are developing a cryptocurrency-friendly regulatory regime by explicitly recognizing the possibility of using public electronic registration mechanisms, such as the Blockchain, for holding and moving financial instruments. This recognition provides greater transparency and certainty to financial market participants and is a means to attract investment in technology companies. Even further down the spectrum are countries such as Belgium, South Africa, and the United Kingdom which have deemed the cryptocurrency market size as too small to cause sufficient concern to warrant regulation or a ban at this juncture.

Finally, on the opposite side of the spectrum lie France, Marshall Islands, Venezuela, the Eastern Caribbean Central Bank (ECCB) member states, and Lithuania, which are seeking to develop their own system of cryptocurrencies.

As shown through the spectrum above, governmental approaches towards cryptocurrency are diverse, varying from reporting for tax purposes, regulation of initial coin offerings (fundraising method used primarily by startups wishing to offer products and services) and tracking money-laundering schemes. Such variance across government policies translate to variance in their effect on the growth of the industry.

Why is Regulation required?

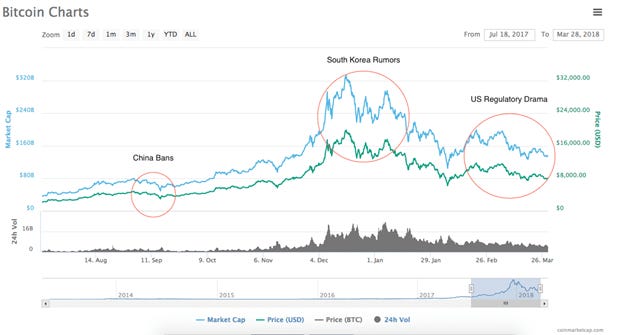

While the initial draw to cryptocurrency for most crypto enthusiasts was its unregulated nature, the same characteristic now hinders its wide-scale adoption. Wei Zhou, the chief financial officer of the major cryptocurrency exchange, Binance, referred to the countries with an unregulated crypto market as the “Wild Wild West”, and that “Innovation comes first, regulation follows”. Such claims in support for crypto regulation stem from the fact that human involvement in the trading, the exchanges, and the initial offerings leaves room for fraud, despite the safety of blockchain technology. Furthermore, concerns of money laundering, terrorism and other organized crime have strengthened the support for development of crypto regulation.

Source: Finance Magnates

As can be seen in the infographic above, major cryptocurrency regulations have surprisingly never impacted the share price of Bitcoin apart from some immediate volatility.

My research showed that crypto users widely share the belief that although regulations might suppress the trading values of cryptocurrency and stifle its innovation in the short term, appropriate regulations will stabilize the market and make crypto a safer investment in the long run. Despite the risk that follows the implementation of regulations, protections for investors are predicted to alleviate outside manipulation.

Recent Regulatory Actions

I have listed nine major regulatory actions that have taken place across the globe during the past year, which signal a mainstream adoption of cryptocurrencies.

European Union (EU) – Proposal for a Regulation on Markets in Crypto-assets (MiCa)

On September 24, 2020, the EU Commission officially released regulations on Markets in Crypto-assets (MiCa) as a part of the wider EU Digital Finance Strategy. The proposed goals are (1) to make financial services more digital-friendly and reduce the rate of cash payments, which currently make up 78% of all payments in the eurozone, and (2) stimulate responsible innovation and competition among financial services providers within the EU.

MiCa proposes to differentiate between crypto-assets that are currently governed by EU legislation and other crypto-assets that fall outside its scope. There are multiple home-grown regulations in the EU that are specific to each country, since crypto-assets and MiCa seek to divert from the Status Quo.

Prof. Rasa Karpandza, a professor of Economics and Finance at New York University Abu Dhabi and EBS Business School, claimed that “In order to achieve widespread usage as an alternative to fiat options, blockchain and crypto assets need to be classified appropriately and this is a good first step” during my interview.

The EU Commission chose to lay down a single set of immediately applicable rules throughout the EU's Single Market (as opposed to a "Directive", which ultimately leaves some level of Member State discretion through the need of national transposition). Therefore, all member states have no choice other than to adopt the MiCa Regulation (once implemented).

Achieving EU market harmonization and prevention of its market regulatory fragmentation is one of MiCa's stated main aims. I believe that MiCa will effectively bring together the fragmented national crypto-asset legal regimes within the EU including Malta, Estonia and France.

United States (US) – Stablecoin guidance

The Securities and Exchange Commission (SEC) published stablecoin guidance on September 21, 2020, providing the first detailed national guidance on how cryptocurrencies backed by fiat currencies should be treated under law. Stablecoin (cryptocurrencies designed to minimize volatility of price and usually backed by fiat money) issuers have been using U.S. banks for years but in an unclear regulatory environment. Through the new guidance, the SEC plans to better ensure safety for the federally regulated banks as they provide services to stablecoin issuers.

Venezuela – Decentralized Exchange

On October 2,2020, the National Superintendency of Securities of Venezuela (Sunaval) authorized the operation of a decentralized electronic exchange in which shares, fiat money, securities, debt securities or cryptocurrencies can be exchanged. The platform plans to decrease the commissions to nearly 0% in order to encourage its use.

Israel – Treatment of cryptocurrency as Fiat

Israeli legislature has proposed on September 22, 2020 the amendment of existing tax law, in order to (1) have digital currencies be treated more like fiat for tax purposes and (2) exempt digital currencies like Bitcoin (BTC) from being subject to capital gains taxes. Under current income tax policy, Bitcoin is treated as an asset and taxed 25% whenever individuals convert their tokens into fiat. The new bill has detailed some properties in order to be considered a currency. Any cryptocurrency that meets the specified criteria, such as Bitcoin and Ethereum, can be considered a currency for both trading and taxation purposes.

Malaysia – Approval of Cryptocurrency exchange

On January 15, 2019, Malaysia passed “The Capital Markets and Services (Prescription of Securities) (Digital Currency and Digital Token) Order 2019”, which was designed to regulate DAX operators. Promptly after the passage, Malaysia’s Securities Commission fully legalized the operation of a cryptocurrency exchange agency. They have taken their cue from Japan, which recently approved their 23rd exchange.

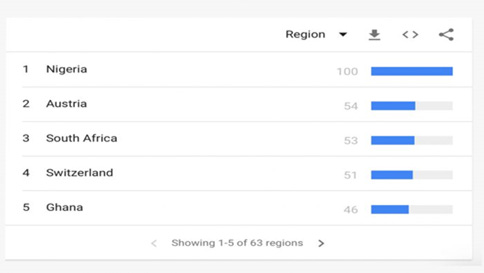

Nigeria – Beginning of regulatory conversation

Source: Google Trends, Regions with highest bitcoin searches

Bitcoin has become increasingly popular in Nigeria (highest google searches in the World) and the Nigerian SEC is making moves toward regulating cryptocurrencies by recognizing them as financial securities. The Nigerian SEC claimed that “the general objective of regulation is not to hinder technology or stifle innovation, but to create standards that encourage ethical practices”, advocating that this will protect investors’ interests and promote transparency.

South Korea – Permit System for Crypto Exchanges

On March 5, 2020, South Korea’s National Assembly passed a revised bill on the reporting and use of special financial transaction information. The bill focuses on the introduction of a permit system for cryptocurrency exchanges as well as the plans to strengthen the Anti-Money Laundering (AML) system for virtual assets such as cryptocurrency.

China – Digital Yuan

Although cryptocurrency is banned in China, digital yuan, now successfully piloted across four cities, has become one of the country’s top priorities. Digital yuan targets the dominance of tech giants, such as Alibaba and Tencent, in the digital payments sector. However, the government remains cautious in its approach to both its own cryptocurrency and digital assets and is yet to issue regulations.

Why are countries so slow with their regulations?

I found that there are largely three reasons behind the slow pace of crypto regulation’s development. The first has been repeatedly mentioned by blockchain enthusiasts on Reddit and Twitter and argues that the absence of regulation is a deliberate economic strategy by many countries. This is because governments believe that strict crypto regulation will hinder growth and innovation. According to the theory, these countries further believe that while high barriers to entry through stricter regulation can benefit users by providing security, it may also curtail potential projects through financial and regulatory strains.

Second, current understanding of cryptocurrency by economists and policymakers is incomplete, partly due to the volatility of the crypto market and its small size compared to other mature financial securities or forex markets. This discourages governments from implementing new regulations and prevents successful expansion of existing laws to target the misuse of cryptocurrency.

Lastly, countries, specifically the developing nations, believe that cryptocurrency will be detrimental to their control over economic function since various transaction will by-pass the central banks. Decentralized finance (more on this in our previous newsletter) has the potential to disrupt the financial services sector thereby enabling the unbanked community (those with no access to financial services either due to geography or social conditions) to access funds.

Perhaps, refraining from involvement with cryptocurrency will benefit these countries by protecting traditional institutions and consumers from money laundering and terrorism. Maybe it will be detrimental to these countries by leaving them behind as other countries experience technological and economic divergence. Only time will tell.

We will continue to follow this story and share any new and exciting trends in the fintech industry next week. If you have any questions, feel free to message me at a.shah@nextrope.com. Hope to see you next week!

I do believe that crypto currencies are the future and proactive governments will use this opportunity for growth. As is clear from the article, developed countries have sensed the opportunity and are steering their digital economies in this direction. It is only a matter of time when the others will have to follow suit. It’s never too early to dive in definitely a good investment for future. Well written article, Ayaan!!